Quick Summary: Publicly-traded companies must disclose disaggregated information about their operating segments. This is just the short executive summary of IFRS 8 and does NOT replace the full standard - you can see ...

Introduction To Segment Reporting - Topic Summary

Main Summary

Publicly-traded companies must disclose disaggregated information about their operating segments. This is just the short executive summary of IFRS 8 and does NOT replace the full standard - you can see ... Operating segments (IFRS 8) - ACCA (SBR) lectures Free ACCA lectures for the Strategic Business

Comparison Notes

Insurance Technology Context related to Introduction To Segment Reporting.

Cost and Benefit Notes

Policy & Claims Notes about Introduction To Segment Reporting.

Planning Tips

Implementation Considerations for this topic.

Important details found

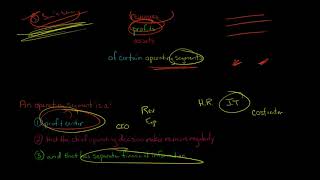

- Publicly-traded companies must disclose disaggregated information about their operating segments.

- This is just the short executive summary of IFRS 8 and does NOT replace the full standard - you can see ...

- Operating segments (IFRS 8) - ACCA (SBR) lectures Free ACCA lectures for the Strategic Business

Why this topic is useful

This topic is useful when readers need a quick overview first, then want to move into supporting details and related references.

Planning Tips

Why do related topics matter?

Related topics can help readers compare alternatives and understand the broader financial context.

What should readers compare first?

Readers should compare cost, expected benefit, risk level, eligibility, timeline, and long-term impact.

What details are most useful?

Useful details often include fees, terms, returns, limitations, requirements, and practical examples.