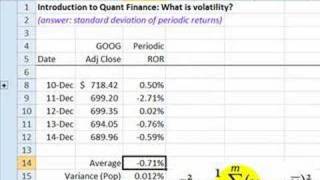

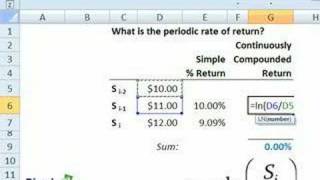

Topic Brief: This is a side-by-side comparison of EWMA and GARCH(1,1) to show their similarities (i.e., both are conditional estimates that ... The basic approach to VaR is delta normal: a scaled standard deviation.

Frm Intro To Quant Finance Volatility - Topic Summary

Main Summary

This is a side-by-side comparison of EWMA and GARCH(1,1) to show their similarities (i.e., both are conditional estimates that ... The basic approach to VaR is delta normal: a scaled standard deviation.

Comparison Notes

Insurance Technology Context related to Frm Intro To Quant Finance Volatility.

Cost and Benefit Notes

Policy & Claims Notes about Frm Intro To Quant Finance Volatility.

Planning Tips

Implementation Considerations for this topic.

Important details found

- This is a side-by-side comparison of EWMA and GARCH(1,1) to show their similarities (i.e., both are conditional estimates that ...

- The basic approach to VaR is delta normal: a scaled standard deviation.

Why this topic is useful

This format is designed to help readers move from a broad question into more specific pages without losing context.

Planning Tips

What should readers compare first?

Readers should compare cost, expected benefit, risk level, eligibility, timeline, and long-term impact.

What details are most useful?

Useful details often include fees, terms, returns, limitations, requirements, and practical examples.

Is this information financial advice?

No. This page is general information and should be checked against official sources or a qualified advisor.